Trust accounting software for South Africa

built for the way agencies are audited.

Per-landlord trust accounts, deposit-only ledgers under PPA section 54, landlord interest-bearing accounts, deposit-interest accrual, and an audit trail structured to align with how property practitioners are inspected.

- Property-practitioner aware

- PPA section 54 aware

- Multi-landlord ready

- Year-end lockable

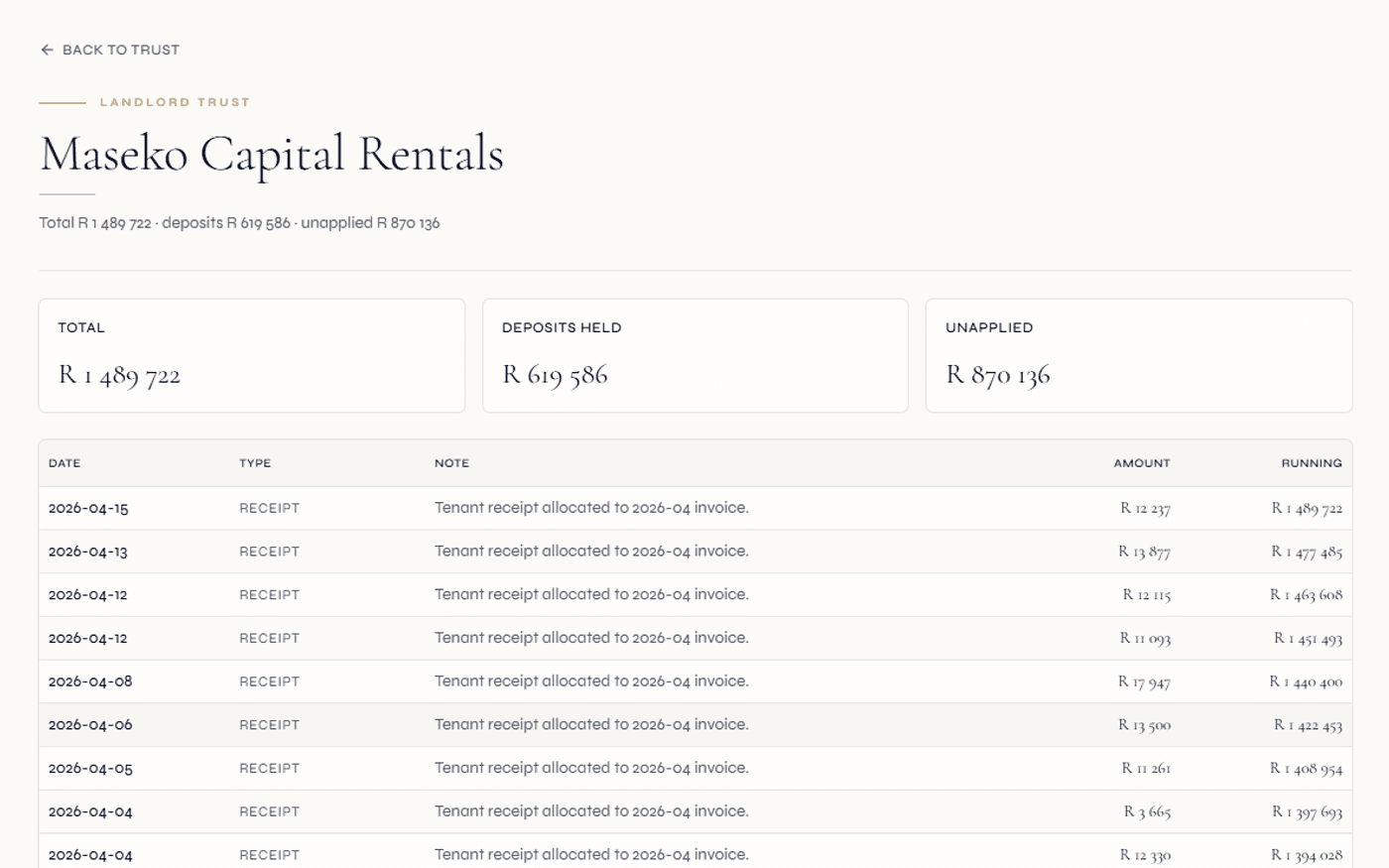

Each landlord has their own trust account, with its own ledger and balance.

Deposits stay in the regulated trust account; rent flows direct to landlord by default.

Lock a financial year once audit is signed off — immutable thereafter.

In South Africa, trust money is regulated money — not operating cash.

If you take a deposit from a tenant, you are temporarily holding someone else's money in trust. That changes the legal character of the cash: it has to be ring-fenced from operating funds, it has to be reconciled, and it has to be auditable. Under the Property Practitioners Act of 2019 (PPA), section 54 enforces this for property practitioners; the Estate Agency Affairs Board (EAAB) historically supervised the same principle.

Most property management software treats trust as a side-account or an external bank link. Regalis treats it as a first-class concept. Each landlord gets their own trust account, every trust movement is recorded as an immutable ledger entry, and the platform actively prevents rent flows from contaminating the deposit ledger.

For a managing agent running multiple landlord books, that means an audit can be answered per landlord, per year, from inside the platform — no spreadsheet reconciliation, no after-the-fact rebuilding of how a deposit moved.

How trust accounting usually goes wrong

- Deposits and rent are held in the same trust account, and the agency cannot tell, at any given moment, which fraction of the balance is deposit money vs. operating money.

- A spreadsheet tracks deposits separately from the actual bank balance, and the two drift apart over time.

- Move-out refunds happen ad-hoc; nobody charges deposit interest because nobody knows what the right number is.

- Year-end reconciliation requires the principal agent to rebuild ledger movements from bank statements, screenshots and accountant emails.

- EAAB audit asks for trust account proof — and the team has to manually pull statements per landlord.

How Regalis does it

- Each landlord has their own regulated-trust account. Balances are queryable on demand and never drift.

- Rent flows default to direct-to-landlord settlement so they never enter the trust ledger by accident.

- Deposit-interest accrual runs monthly per lease, with the rate stored on the trust account itself.

- Reconciliation runs are first-class records with exception tracking and resolution workflow.

- The financial year can be locked once audit is signed off, after which no edits are possible.

From the deposit receipt to a clean audit.

Deposit comes in

A tenant pays a deposit at lease signing. The receipt is captured against the lease and written to the regulated trust account for that landlord. A structured audit trail from the first cent.

- Receipt linked to lease

- Regulated trust account per landlord

- Immutable ledger entry

Interest accrues monthly

Interest accrues monthly per lease using the rate stored on the trust account. Non-destructive — the deposit principal is untouched.

- Monthly automated accrual

- Per-lease interest record

- Rate configured per trust account

Move-out triggers finalisation

When a lease ends, the move-out workflow computes deductions and refund. Unpaid interest is netted into the refund automatically; the trust balance updates the same instant.

- Section 5 RHA interest applied

- Deductions + refund handled together

- Trust balance updated live

Year-end is reconcilable and lockable

Annual reconciliation walks the year's ledger, surfaces exceptions, and produces a per-landlord trust statement and audit pack. Once audit signs off, the financial year locks — every entry inside it becomes immutable.

- Annual reconciliation per landlord

- SARS-ready tax pack export

- Year-end lock with audit stamps

Everything the regulation expects you to have.

Per-landlord trust accounts

One trust account per landlord. Run 50 landlord books and you get 50 distinct trust ledgers, all rolled up into one agency view.

Deposit-only regulated ledger

The regulated trust ledger sees deposit movements only — deposit in, deposit out, fees, reversals. Nothing else touches it.

Landlord interest-bearing accounts

Optional landlord-owned interest-bearing accounts for landlords who want a savings vehicle held by your agency on their behalf.

Immutable trust ledger

Every entry is append-only. Reversals are explicit, referencing the original — no edits, no deletes, no rewrites.

Deposit interest accrual

Interest accrues monthly per lease using the rate stored on the trust account. Visible per lease and per period.

Rent / trust separation

Rent defaults to direct-to-landlord settlement. The trust ledger is only ever touched for deposit movements, never for monthly rent.

Reconciliation runs

Periodic reconciliation runs surface exceptions — unmatched bank transactions, unallocated receipts, over-allocations, balance mismatches — with a resolution workflow.

Annual reconciliation

Year-end reconciliation rolls per-landlord summaries, stores them as PDF, and locks the financial year on sign-off.

Year locking

Once a financial year is locked, no receipt, allocation or ledger entry inside it can be edited — by anyone.

Why we changed the default to direct-to-landlord rent settlement.

PPA section 54 — read carefully — distinguishes between money received "in trust" and money received as agency operating revenue. Deposits are textbook trust money. Monthly rent, depending on the mandate, can either flow through trust on its way to the landlord, or be settled direct-to-landlord with the agency only retaining their commission.

In an EAAB-supervised world it was common to route every rand of rent through the agency trust. After the PPA came into force, more agencies have moved toward direct settlement, both because it reduces audit surface and because it gives landlords cleaner cashflow.

Regalis defaults each lease to direct-to-landlord rent settlement precisely because that is the cleanest split. The trust ledger only sees deposits. Rent flows are operational. If you need the legacy "everything-through-trust" mode you can configure it per property — but most teams find the direct mode dramatically simplifies their PPA reporting.

Continue exploring how Regalis handles the rest of the rental operation.

Rental arrears collection

When rent does not come in, the arrears workflow handles reminders, retries and the evidence pack.

Read morePOPIA & PAIA compliance

Trust accounting feeds into the broader compliance surface — POPIA retention, breach templates, PAIA manual.

Read moreLandlord portal

Landlords see their own trust balance, statements, and expected payouts in their portal — no separate request needed.

Read moreCommon questions about trust accounting.

Is the trust accounting designed for South African property-practitioner requirements?+

Yes. Each trust account is either a regulated trust (deposit-only, structured to align with PPA section 54) or a landlord interest-bearing account. Deposits and rent flows stay separated, so an audit can focus on the regulated ledger.

How does the deposit-only trust ledger work?+

A deposit comes in, the ledger records it. At move-out, deductions and the refund record out. Every entry is immutable, linked to the lease and tenant, and timestamped. Balances per landlord are visible at any time.

Does each landlord get their own trust account?+

Yes — one per landlord. A managing agent running 30 landlord books has 30 distinct trust ledgers and 30 distinct balances, all rolled up into one consolidated agency view. Per-landlord reconciliation, statements and audit work happen without manual splitting.

Can deposit interest be accrued automatically?+

Yes. Interest accrues monthly per lease using the rate stored on the trust account. At move-out, unpaid interest is netted into the refund automatically, helping you meet the deposit-interest obligations in section 5 of the Rental Housing Act.

How is rent kept separate from trust money?+

Rent defaults to direct-to-landlord settlement, so it never enters the trust ledger. The trust ledger only ever sees deposit movements — a split structured to align with PPA section 54.

Are reconciliations supported?+

Yes. Periodic reconciliation runs surface exceptions (unmatched bank transactions, unallocated receipts, over-allocations, missing entries, balance mismatches) with a resolution workflow. Annual reconciliation rolls up into the year-end record and the financial year can be locked once audit signs off.

What about backups and disaster recovery?+

Scheduled database backups run continuously, written to cloud blob storage with optional restore verification. Once a financial year is locked, every receipt, allocation and ledger entry inside it becomes immutable.

See everything built for you — explore the property managers hub

Trust money is not

operating cash.

Talk to us about migrating your trust ledger into a structure designed to support PPA section 54 and to help you prepare for a property-practitioner audit.