HOA accounting software for South Africa

Homeowners Association accounting, done right.

Run the financial side of a Homeowners Association on one ledger — levy roll from the constitution, per-owner statements, reserve and maintenance fund planning, arrears with interest and budget-vs-actual — on the same platform that runs your rental book.

- Constitution-driven levy roll

- Reserve + maintenance funds

- Arrears + interest

- Auditor-ready ledger

Per-unit levies computed from the share or participation basis set in the HOA constitution against the approved budget.

Operating and reserve / maintenance funds flagged at the chart-of-accounts level — never blurred, always reportable on their own.

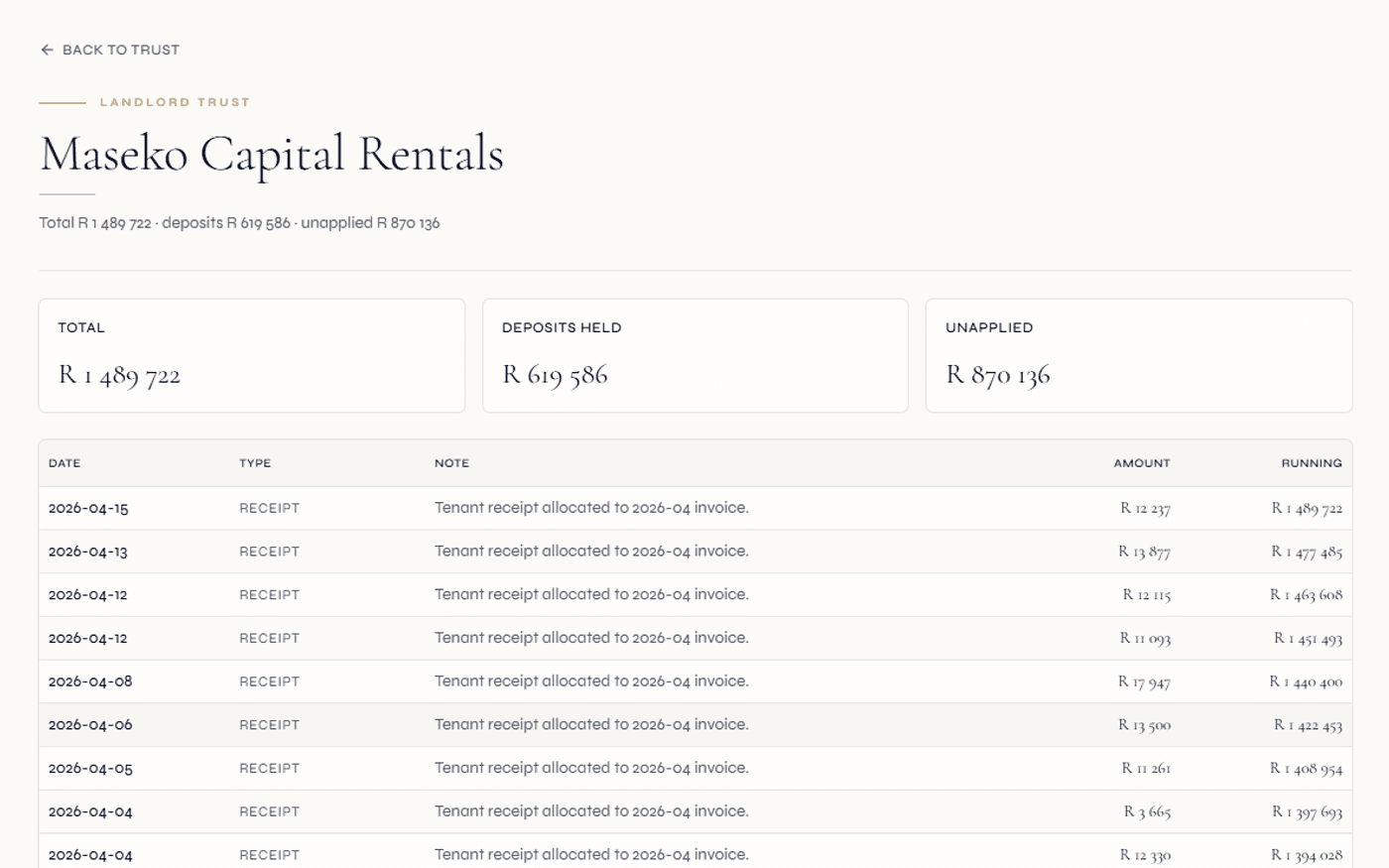

Trial balance, GL and per-owner statements from one ledger. Lock the financial year once audit signs off; entries become immutable.

An HOA is governed by its constitution, not by the STSMA. Its books should reflect that.

A sectional title body corporate is a creature of statute: the Sectional Titles Schemes Management Act (STSMA, 2011) tells it how to govern, and section 3(1)(b) requires it to maintain both an administrative fund and a reserve fund. A Homeowners Association is different. Most HOAs in South Africa are common-law associations of persons, or Non-Profit Companies under the Companies Act, governed by their own constitution or memorandum of incorporation. The levy basis, the fund split and any reserve policy are whatever that founding document sets — not a fixed statutory formula. (Informational only — not legal advice; confirm your scheme's legal form with your own adviser.)

That distinction matters for the accounting. HOA levies might be charged as an equal share, weighted by erf size, or by a participation percentage written into the constitution. The reserve or maintenance fund might be mandated, optional, or replaced by a special-levy-on-demand approach. Generic body-corporate software assumes the STSMA shape and fights you when your constitution says otherwise. Regalis lets the HOA model its own basis, its own fund structure and its own interest-on-arrears policy, then runs the levy roll, the statements and the reports off that.

For a managing agent, the upside is that the HOA's books live on the same instance as the rental trust accounting — one chart of accounts to audit, one ledger, one reconciliation posture. The committee gets clean owner statements and a reserve-fund report; the auditor gets a trial balance and general ledger that already tie out; and nobody is rebuilding the year in a spreadsheet at AGM time.

What HOA finance on spreadsheets costs you

- The levy roll is a spreadsheet that someone re-keys each year — a single broken formula mis-bills every owner.

- Operating money and reserve money sit in one mental pile; nobody can show the committee how the maintenance fund is actually tracking.

- Arrears interest is calculated by hand, if at all, so overdue owners are under-charged and recovery has a weak paper trail.

- Owner statements are produced one PDF at a time, and the figures rarely agree with the bank.

- At year-end the auditor asks for a trial balance and a general ledger that the spreadsheet simply cannot produce.

- When an HOA unit is also being rented out, the levy flow and the rent flow live on different systems and only reconcile by hand.

What a real ledger gives the committee

- A levy roll computed live from the constitution's basis and the approved budget — change the budget, the roll follows.

- Operating and reserve / maintenance funds flagged at the COA level, each reportable on its own at any moment.

- Arrears bands with interest accrued automatically where the constitution permits, posted to the owner ledger.

- Per-owner statements generated in bulk straight from the ledger, so the numbers always reconcile to the cashbook.

- Trial balance, general ledger, income statement and reserve-fund report out of the box for a clean audit handover.

- An HOA unit being rented out shows both the owner ledger and the active lease on one record — levy and rent reconcile cleanly.

From the budget to a clean audit.

Set the levy basis and the budget

Capture how the constitution charges levies — equal share, erf-size weighting or participation percentage — and install the HOA chart of accounts. Draft the annual budget, monthly amounts per line, including any reserve or maintenance contribution, and submit it for committee approval.

- Levy basis per the constitution

- Reserve / maintenance fund line in the budget

- Budget draft → committee approved

Run the levy roll each month

On the 1st of every month the levy run mints an invoice per unit from the basis and the active budget. Special levies for one-off projects layer in on demand with a target unit list. Pro-rata is computed automatically when a transfer of ownership falls within the period.

- Automated monthly levy run

- Special levies on demand

- Pro-rata on mid-month transfers

Collect, allocate and charge arrears

Owner payments arrive by EFT, DebiCheck, card or staff capture and the allocation engine matches them to the right invoice. Overdue balances move into arrears bands; where the constitution permits, interest accrues on the outstanding amount and posts to the owner ledger.

- One allocation engine, all payment paths

- Arrears bands (30/60/90+)

- Interest on overdue levies posted to ledger

Report, reconcile and lock the year

Budget-vs-actual runs continuously. The reserve-fund movement report shows whether the long-term fund is tracking to plan. At year-end the trial balance, general ledger, income statement and per-owner statements come straight from the ledger; lock the financial year once the auditor signs off.

- Budget vs actual + variance

- Reserve-fund movement report

- Per-owner statements + year-end lock

The full financial toolkit for a Homeowners Association.

Every money-touching record links to the right general-ledger line, so the levy roll, the statements and the reports all come from one ledger — not three reconciled spreadsheets.

Constitution-driven levy roll

Per-unit levies computed live from the basis the constitution sets — equal share, erf-size weighting or participation percentage — against the approved annual budget.

Owner records + statements

Each owner has a ledger of invoices, receipts, interest and adjustments. Per-owner statements generate in bulk, reconciled to the cashbook. An owner who rents elsewhere is the same record across contexts.

Reserve + maintenance funds

Reserve and maintenance accounts are flagged at the chart-of-accounts level; movements write to a dedicated ledger so the operating fund and the long-term fund never blur together.

Chart of accounts

Hierarchical chart of accounts with reusable templates and per-property overrides. Every record links to the right GL line for clean general-ledger reporting.

Budget + budget vs actual

Annual budget per HOA with monthly amounts per line. Actual-vs-budget reporting shows month-by-month, YTD, variance and percentage drift — including the reserve contribution.

Arrears + interest

Overdue balances banded by age. Where the constitution permits, interest accrues on the outstanding amount and posts to the owner ledger, with recovery costs raised on the same record.

Receipting + allocation

EFT, DebiCheck, card and manual receipts all feed one allocation engine that matches each payment to the right invoice. A per-bank-account cashbook with allocation rules keeps recon tidy.

Trial balance + general ledger

Once the chart of accounts is installed, the trial balance and GL come automatically from the unified ledger. One source, two reports, both auditor-ready.

Cashbook + bank recon

Per-bank-account cashbook with a hide-allocated toggle, allocation rules per HOA, and bank-feed import. Reconciliation surfaces unmatched and unallocated items for resolution.

Special levies

One-off levies for security upgrades, road resurfacing or reserve top-ups run through the same engine with a one-off flag and a target unit list, charged straight to owner ledgers.

Year-end lock + immutability

Lock the financial year once the auditor signs off. Every receipt, allocation and ledger entry inside a locked year becomes immutable, with scheduled backups behind it.

Conduct charges to ledger

Where the HOA raises a fine or penalty under its conduct rules, the charge auto-posts to the owner ledger so it flows into the same statement and arrears view as levies.

HOAs sit under common law and a constitution — accurate accounting respects that.

It is worth being precise about where an HOA sits. A sectional title body corporate is established and regulated by the Sectional Titles Schemes Management Act, and the Community Schemes Ombud Service Act (CSOS, 2011) brings most community schemes — including many HOAs that meet the definition of a "community scheme" — under CSOS oversight and the CSOS levy. But the HOA's internal financial rules — how levies are struck, whether a reserve fund is held, how interest on arrears is charged — flow from its own constitution or memorandum of incorporation, not from STSMA section 3(1)(b).

Regalis is built to honour that. The reserve and maintenance funds are modelled as flagged ledgers rather than as a fixed statutory split, so the HOA can run the fund structure its constitution actually mandates. CSOS registration is a first-class field where the scheme falls under CSOS, and CSOS levy obligations surface in the compliance planner. The owner ledger, the trust posture and the audit trail line up to the way an auditor and, where relevant, the Community Schemes Ombud expect to see the books.

None of this is legal advice. The right answer for any given estate depends on its founding documents and whether it meets the CSOS community-scheme definition — confirm that with your own attorney or auditor. What Regalis is designed to do is follow the shape you decide on faithfully and report cleanly once it is set.

Continue exploring how Regalis handles the rest of the rental operation.

HOA management

The operational side of the HOA — conduct-rule offences, transfers, gate access codes, AGM documents and recurring estate maintenance.

Read moreLevy collection

Structured levy arrears recovery — DebiCheck mandates, multi-channel reminders and a structured evidence trail designed to support CSOS dispute preparation.

Read moreBody corporate accounting

The STSMA-governed counterpart — statutory administrative and reserve funds under section 3(1)(b) for sectional title schemes.

Read moreTrust accounting

Per-landlord, deposit-only trust ledgers under PPA section 54, with an EAAB-aligned audit trail on the same instance.

Read moreCommunity scheme management

The full community-scheme platform — HOA, body corporate, sectional title and share block, integrated with rentals.

Read moreCommunity schemes software

One platform for every scheme type — levy roll, trustee multi-sig, reserve fund segregation and CSOS compliance.

Read moreCommon questions about HOA accounting.

What does HOA accounting software actually do?+

It runs the financial side of a Homeowners Association: it computes the levy roll from each unit's share or participation basis, mints monthly levy invoices, posts owner receipts, charges arrears interest, tracks the operating and reserve funds separately, and produces budget-vs-actual, trial balance, general ledger and per-owner statements for the annual audit.

How is HOA accounting different from body corporate accounting on Regalis?+

The mechanics overlap, but the governance differs. A sectional title body corporate is statutory — its reserve fund and financial rules come from the Sectional Titles Schemes Management Act (STSMA s3(1)(b)). A Homeowners Association is usually a common-law association governed by its own constitution or a Non-Profit Company under the Companies Act. Its levies, fund split and reserve policy are whatever the constitution sets, not a fixed statute. Regalis lets the HOA model that on its own terms. For the statutory body corporate flow, see our body corporate accounting page; this page covers the constitution-driven HOA case. Informational only — not legal advice.

How is the HOA levy roll calculated?+

The levy roll is computed live from each unit's levy basis — an equal share, an erf-size weighting or a participation percentage set in the constitution — against the approved annual budget. Owners see their own per-unit balance; the committee sees the full roll with arrears bands. Special levies for one-off projects use the same engine with a one-off flag and a target unit list.

Does it handle the reserve / maintenance fund?+

Yes. Reserve-fund and maintenance-fund accounts are flagged at the chart-of-accounts level and their movements write to a dedicated ledger, so the operating fund and the long-term fund never blur together. Where the constitution mandates a reserve contribution, you budget for it as a line and it flows through the monthly levy run; budget-vs-actual then shows whether the fund is tracking to plan.

How are arrears and interest on overdue levies handled?+

Overdue owner balances surface in arrears bands (current, 30, 60, 90+ days). Where the constitution permits interest on overdue levies, the platform accrues it on the outstanding balance and posts it to the owner ledger, so a follow-up statement reflects the levy, the interest and any recovery costs already raised. The structured recovery workflow itself lives on the levy collection page.

What financial reports come out at year-end?+

Once the chart of accounts is installed, the trial balance and general ledger come automatically from the unified ledger. On top of that you get an income statement, budget-vs-actual with variance and percentage drift, a reserve-fund movement report and per-owner statements. The financial year can be locked once the auditor signs off, after which entries inside it are immutable.

How do owners pay, and how are receipts allocated?+

Owners pay by EFT matched through the bank feed, by DebiCheck mandate, by card or EFT through the owner portal, or by manual receipt capture by staff. Every path feeds the same allocation engine, which matches the receipt against the right invoice on the owner's ledger. A per-bank-account cashbook with allocation rules keeps reconciliation tidy.

Can a managing agent run HOA accounting alongside its rental trust accounting?+

Yes. An HOA runs in scheme mode on the same instance that runs the firm's rental book. The same finance hub, the same trust-ledger posture and the same team directory serve both. An owner who also rents elsewhere is one record across both contexts, and firm-wide arrears — levy plus rent — show on one view.

Stop rebuilding the year in a spreadsheet.

One ledger, one clean audit.

Walk through the levy roll, the reserve-fund reporting, the arrears workflow and the per-owner statements with someone from the team.